Designed exclusively for doctors and their employees

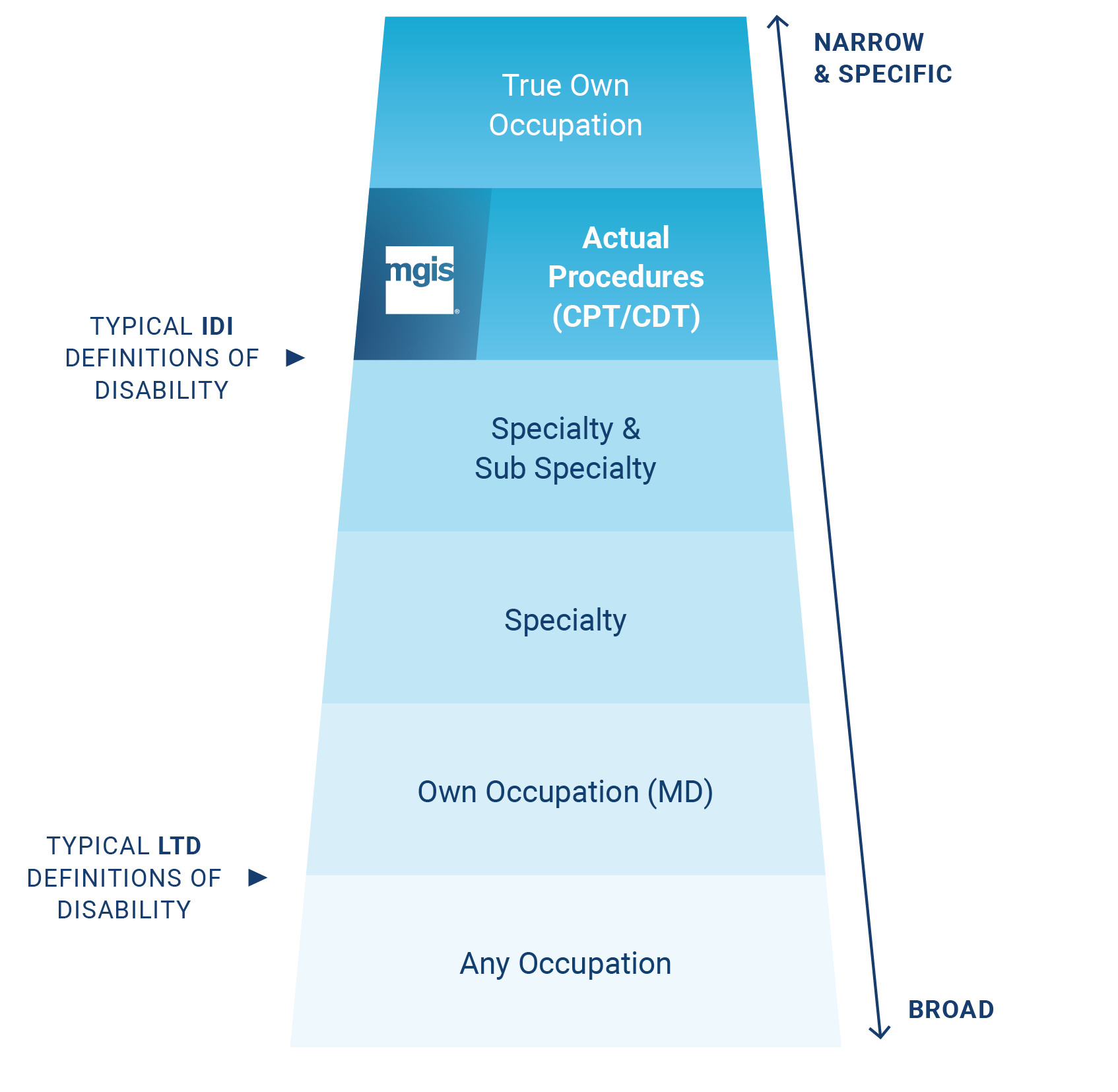

Doctors have specialized requirements for income protection not addressed by typical group disability insurance solutions.

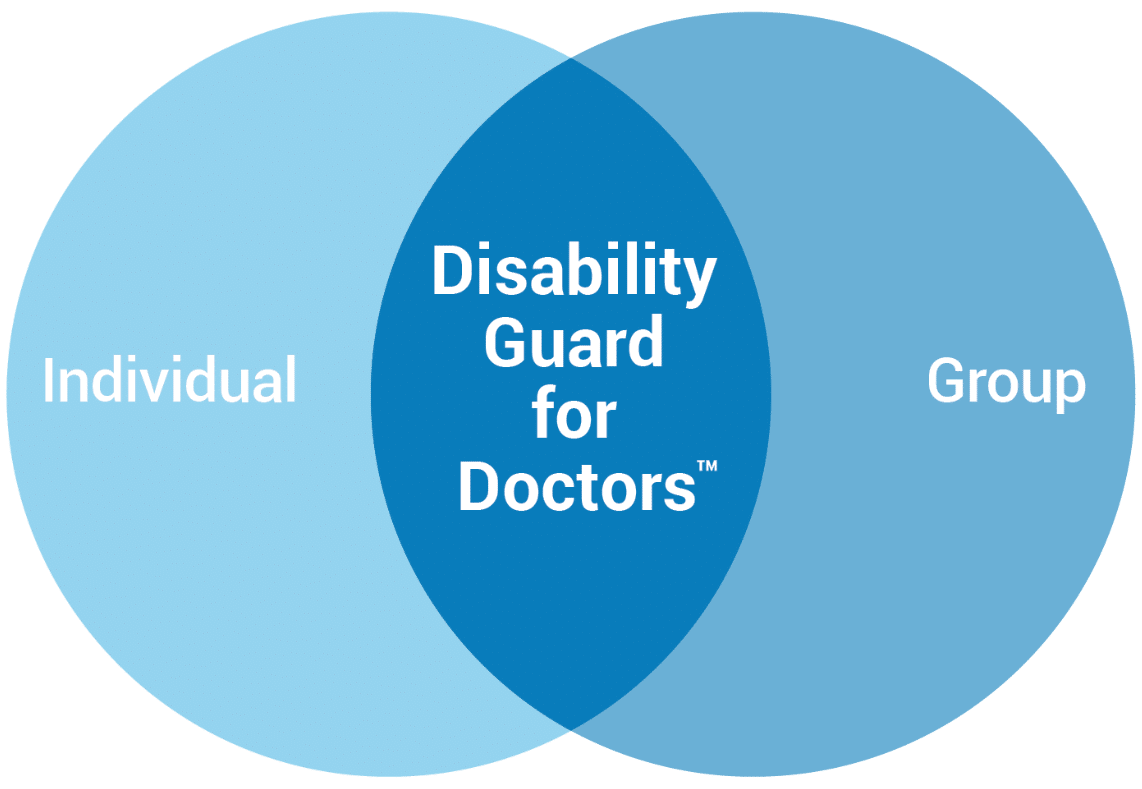

This unique disability insurance includes highly valued individual disability policy provisions, but with guaranteed issue and simplified administration. In essence, Disability Guard for Doctors™ offers you the best of individual disability insurance (IDI) and group long-term disability (LTD) in one package.

Download All

Download All